A new survey made by Quest TechnoMarketing shows how servo suppliers' market shares in the German machinery industry developed from 1999 to 2013.

(1888PressRelease) January 21, 2014 - The results of this survey are currently published in the Quest Trend Magazine. They are based on three representative market surveys regarding the use of servo drives in the German mechanical engineering industry carried out by Quest TechnoMarketing in the years 1999, 2006 and 2013.

The results document two contradictory tendencies of variety of the suppliers and their concentration in the use.

The variety appears by the fact that the number of main suppliers of servo converters with the machine-builders doubled in the 15 years from 1999 to 2013. So innovations and product differentiation in the servo market open new applications with the machine-builders that can be operated even by smaller suppliers.

The analysis divides the servo suppliers into three groups, i.e. the group of servo suppliers used with 10% and more machine-builders, the group with a market share of over 5% but below 10% and finally the group with a market share of 5% and less.

This structural analysis makes the effect of the concentration in the use of servo suppliers visible. Because in the year 2013 each second machine-builder of servo converters used suppliers with 10% and more market share. Since 2006 more machine-builders have been relying on relatively fewer and larger servo suppliers. The group of these servo suppliers covers 2013 in alphabetical order Lenze, SEW and Siemens.

Each sixth machine-builder used servo suppliers with over 5% and below 10% market share. This group of the servo suppliers showed a stable position with the machine-builders.

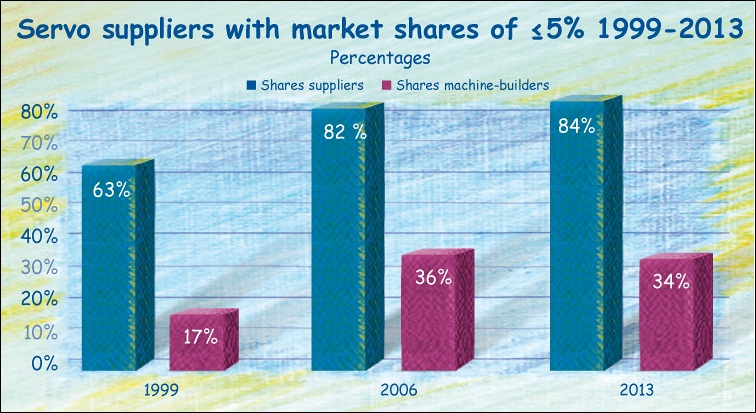

A third of the machine-builders preferred servo suppliers with a market share of 5% and less. This group strongly increased their proportion at all denominated servo suppliers from 63% to 84% in the course of 15 years. Here the duplication of the supplier denominations came fully into effect. Even the tendency showed up that a little fewer machine-builders used a larger variety of servo suppliers.

So concentration as well as differentiation is the two trends that were formed by the machine-builders deciding on servo suppliers.

The article is published on http://www.quest-trendmagazin.de/Marktanteile-Servolieferanten.269.0.html?&L=1.

A new survey made by Quest TechnoMarketing shows how servo suppliers' market shares in the German machinery industry developed from 1999 to 2013.

A new survey made by Quest TechnoMarketing shows how servo suppliers' market shares in the German machinery industry developed from 1999 to 2013.

Satisfied Users &

Satisfied Users &  Approved Press Releases

Approved Press Releases